Ultra-Long-Range vs. Charter: Why the Sealed‑Bid Model Is Reshaping Private Jet Ownership

The private aviation market is undergoing a subtle, consequential shift. Traditionally, the decision to fly privately has been framed as a choice between owning (outright or fractional) an ultra‑long‑range (ULR) jet versus using on‑demand charter. Today, a newer transactional mechanism — the sealed‑bid model for buying and selling pre‑owned business jets — is changing how owners, buyers, and charter operators think about asset allocation, liquidity, and risk. This article explains the core differences between ULR ownership and charter, outlines how the sealed‑bid model works, and analyzes why sealed bids are reshaping private jet ownership economics and behavior.

Ultra‑Long‑Range Ownership vs. Charter: The basics

- Ultra‑Long‑Range ownership

- Definition: ULR jets are aircraft capable of nonstop flights on the longest business routes (e.g., New York–Singapore, London–Los Angeles) with full payloads. Examples include Dassault Falcon 7X/8X, Gulfstream G650/G700, and Bombardier Global 7500.

- Value proposition: Ultimate convenience, privacy, time savings, and scheduling control. For certain corporate users and high‑net‑worth individuals, owning a ULR jet is about mission capability (nonstop intercontinental travel), brand/status, and guaranteed availability.

- Costs and considerations: High capital expenditure, substantial fixed costs (hangar, crew, maintenance reserves), depreciation exposure, and lower utilization efficiency unless the owner flies many long segments annually.

- Charter (on‑demand)

- Definition: Renting an aircraft as needed via brokers, operators, or membership programs. Charter provides access to a wide range of aircraft types, from light jets to ULRs.

- Value proposition: Flexibility without asset ownership, variable cost tied to usage, no direct exposure to resale risk, and potential access to jets otherwise unaffordable for ownership.

- Costs and considerations: Higher per‑flight marginal cost compared with an efficiently used owned jet; availability for ULR legs can be limited and expensive; quality and consistency depend on operator network and market demand.

Why asset ownership still matters

Owning a ULR jet remains compelling for specific use cases: executives who value guaranteed nonstop scheduling, owners who need privacy/security for sensitive missions, and lifestyle buyers who treat aircraft as part of their personal operations. Yet ownership is a capital‑intensive commitment with resale and liquidity risk. Those frictions are precisely where market innovation — particularly sealed‑bid resale mechanisms — is having an outsized influence.

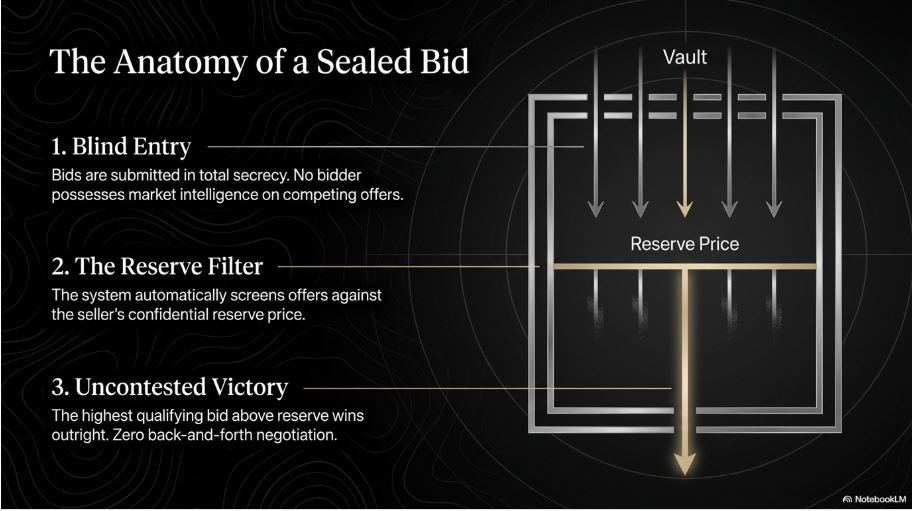

What is the sealed‑bid model?

- Mechanism: Sellers (often owners or brokers) put an aircraft for sale and invite confidential offers within a fixed window. Prospective buyers submit their highest price without knowing competing bids. After the window closes, the seller (or auction manager) evaluates offers and selects one — sometimes the highest, sometimes based on other terms.

- Variants: Pure sealed‑bid auctions, sealed offers with reserve prices, and hybrid processes that include a short negotiation phase after bids are revealed to the seller.

- Participants: Private buyers, institutional investors, charter operators expanding fleets, and specialists who acquire aircraft for placement in fractional or charter programs.

Why sealed bids matter to the private jet market

- Improved price discovery

- Pre‑owned business jet pricing can be opaque and influenced by limited comparable sales, infrequent transactions, and emotional owner pricing. Sealed bids aggregate real‑time market willingness to pay, reducing guesswork and narrowing the gap between seller expectations and buyer reality.

- Greater liquidity and faster transactions

- Sellers facing uncertain resale timelines can use sealed‑bid events to generate multiple offers quickly. A compressed bidding window often produces faster deal flow than drawn‑out private negotiations, enabling owners to redeploy capital or exit depreciating assets sooner.

- Reduction in listing bias and market theatrics

- Traditional listings (long market exposure, price reductions, staged open houses) can stigmatize an aircraft and force sellers to accept lower prices. Sealed bidding preserves confidentiality and avoids public perception penalties that arise from “days on market” metrics.

- Enables new buyer types and fleet strategies

- Charter operators and fleet managers can use sealed bids to acquire ULRs opportunistically when they appear at attractive valuations. That makes it more practical to expand ULR charter capacity without committing to premium initial pricing or prolonged negotiations. Conversely, investors looking to capture residual value can bid strategically in sealed auctions.

- Aligns incentives for risk transfer

- Many owners balk at the idea of selling at “market” precisely because market is hard to measure. A sealed‑bid event puts the market on the table; buyers bear the pricing risk in their submitted bids, and sellers gain certainty about the best current offer. This more explicit risk allocation smooths transaction dynamics.

Impacts on the ULR vs. Charter decision

- For current and prospective owners

- Reduced upfront and ongoing uncertainty about resale values makes ownership more palatable for certain buyers, particularly those who balance personal use with potential occasional chartering to offset costs.

- Improved exit mechanisms lower the effective risk premium owners demand, narrowing the economic gap between ownership and charter when utilization is borderline.

- For charter operators

- Sealed bids provide a tactical tool to acquire ULRs at prices that can make new long‑range routes commercially viable. That can expand the ULR charter supply, improving availability for end users and putting downward pressure on per‑flight charter rates for long legs.

- Operators can also flip aircraft into or out of their fleet more easily, aligning capacity with seasonality and demand spikes.

- For buyers who prefer charter

- Greater ULR supply in the charter market may reduce waiting times and premium surcharges for long nonstop legs. As charter operators grow fleets opportunistically through sealed bids, the option value of charter relative to ownership improves.

Risks and limits of the sealed‑bid model

- Bid blindness and overpay risk: Buyers can overpay if they lack comparable market intelligence or if a small number of strategic buyers drive bids up. Due diligence remains crucial.

- Asymmetric information: Sellers with better understanding of maintenance history, utilization, and records can structure auctions to attract less informed bidders while retaining superior negotiation power.

- Not a panacea for highly bespoke jets: Ultra‑customized interiors or owner‑specific modifications may still require longer, negotiated sales channels to find a buyer who values those attributes.

- Legal and contractual complexity: Aviation sales involve regulatory approvals, liens, maintenance records, import/export considerations, and escrow arrangements. Sealed bids speed price discovery but must be followed by robust transactional processes.

Practical considerations for participants

- Sellers should prepare comprehensive, transparent records: full logs, inspections (pre‑sale AD and SB checks, pre-buy-friendly reports), paint/interior status, and clear lien searches. Better data reduces buyer uncertainty and improves bid quality.

- Buyers should set disciplined bid strategies: establish a valuation cap, account for potential refurbishment and transfer costs, and include logistical timelines. When competing for ULRs, factor in potential revenue if the aircraft will be used in charter.

- Use trusted intermediaries: brokers and auction managers who specialize in business jets can structure reserve prices, vet bidders, and manage escrow and closing to reduce transactional risk.

- Consider hybrid approaches: sealed bids followed by short negotiation windows can balance confidentiality with the ability to refine terms when needed.

Looking ahead: market implications and strategic takeaways

- More dynamic secondary market: As sealed‑bid mechanisms become normalized, pre‑owned inventory that previously lingered on the market could circulate faster. That dynamism supports an ecosystem where ownership and charter coexist more fluidly.

- Better matching of supply and demand for ULR capacity: Operators can scale ULR offerings opportunistically, making long‑range charter more accessible and affordable. This reduces one of charter’s historic weaknesses — limited ULR availability — and narrows the gap between charter convenience and ownership guarantees.

- Evolving buyer profiles: Some buyers who previously hesitated to own ULR jets because of resale uncertainty may now view ownership as a manageable capital decision. Conversely, some owners who prioritize capital flexibility may lean more on charter, knowing they can achieve timely exits through sealed bids.

The sealed‑bid model is not a wholesale replacement for negotiated sales or traditional brokerage, nor does it change the fundamental tradeoffs between owning an ultra‑long‑range jet and using charter. What it does deliver is more transparent, faster price discovery and a clearer mechanism for transferring ownership risk. Those benefits make ownership more attractive to some and charter more viable to others by altering liquidity dynamics and enabling fleet strategies that previously were logistically or economically impractical.

For buyers, sellers, and charter operators, the lesson is pragmatic: treat sealed bids as another strategic tool. When used properly — with solid records, disciplined valuation, and professional intermediaries — sealed bids can reduce frictions, unlock value, and ultimately reshape the economic calculus that drives decisions between ULR ownership and charter.

About The Miccoli Group

Maria Miccoli is also the CEO and Editor-In-Chief of TheMiccoliGroup.com and the company behind closedbid.com/air — a sealed bid acquisition intelligence platform for private jets, corporate jets, and

helicopters. The sealed bid auction platform air.closedbid.com is a dedicated vertical for private and corporate jets, helicopters and other aviation vehicles. For media inquiries and broker or buyer registration visit Closedbid.com/Air/Contact .